Quick Look: BABA

Still alive.

Here is a good summary by DBS HK:

Alibaba is China’s largest e-commerce platform company, with Taobao and Tmall having monthly active users (MAUs) of over 800 million. It has an extensive e-commerce ecosystem including Alipay, Cainiao Logistics, and AliCloud. Its revenue is derived from e-commerce (86%), cloud computing (8%), digital media & entertainment (5%) (i.e., Youku, Tudou, and UCWeb), and innovation initiatives and others (1%) (i.e., Dingtalk and AutoNavi).

Leading e-commerce player in China with 42% market share. Alibaba is the largest e-commerce player in China, operating Taobao and Tmall. It has lost significant market share to PDD and livestreaming platforms in China, dropping from 52% in 2021 to 42% in 2023. However, Taobao & Tmall’s GMV are recovering, recording double-digit growth in its recent Double-11 promotion. Apart from its core e-commerce business, the company also derives revenue from cloud computing, digital media & entertainment (e.g., Youku and Tudou), and other innovation initiatives (e.g., Dingtalk).

International commerce is the key growth engine. Alibaba's international commerce platforms – AliExpress, Lazada, and Trendyol—account for c.11% of total revenue. We expect the segment to record a 23% CAGR from FY3/24 to FY3/27F. Meanwhile, Alibaba Cloud leads the cloud services market in China with a c.37% market share. We expect cloud revenue to generate a solid 11% CAGR from FY3/24 to FY3/27F, supported by increasing demand from public cloud and AI-related products.

CMR is the key share price catalyst. Taobao and Tmall account for 46% of the group’s revenue, and thus customer management revenue (CMR) is a key share price driver. We project CMR growth would accelerate to 5% and 6% in 3QFY3/25 and 4QFY3/25 (vs. 1%/2% growth in the previous two quarters), thanks to the introduction of a software service fee of 0.6% of GMV and the launch of its platform-wide advertising solution. We expect the company’s adjusted earnings to bottom in FY3/25 and grow by 9% in FY3/26, with EBITA margins for Taobao and Tmall stabilizing at c.42% and improving profitability in its cloud business.

(1) Policy risks from regulators; (2) intense competition from other e-commerce platforms; and (3) earnings drag from investments in new initiatives.

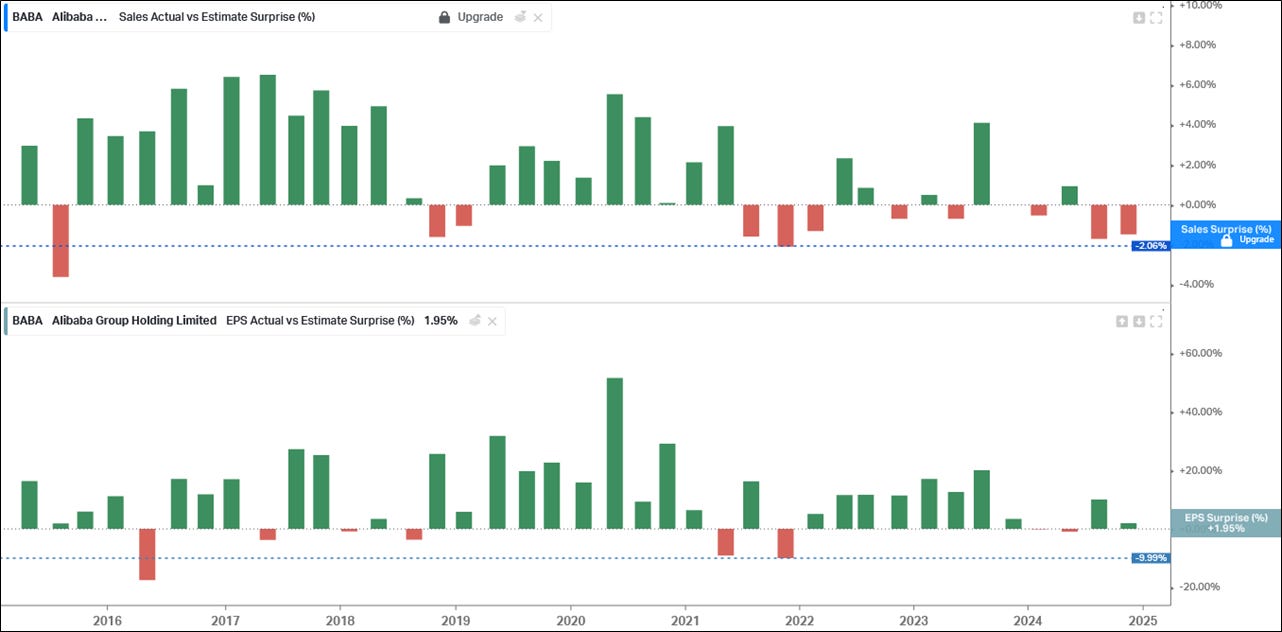

Modelability

Alibaba doesn’t miss by much versus the consensus revenue and EPS estimates, especially annually. This shows that it can be modeled with relative accuracy.

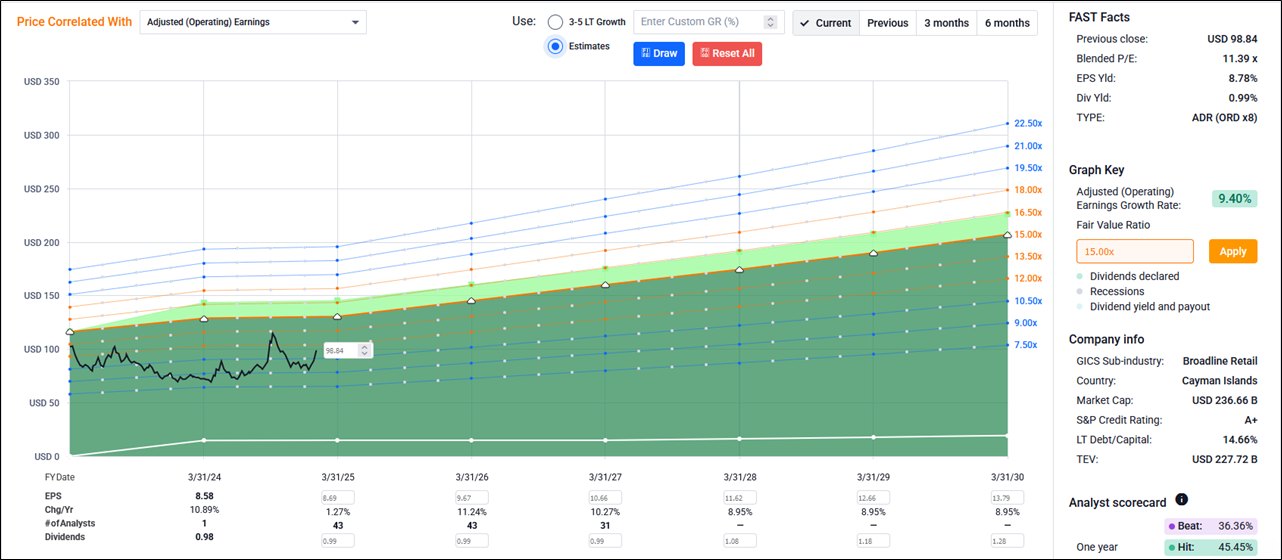

Valuation

It has traded around a 26 PE since its IPO in 2014 with 15% EPS growth. It currently trades around 11 P/E.

Alibaba is projected to grow around 10% in the next 5 years.

If it keeps trading at an 11 P/E, then returns would be around 50% total or 9% annually in the next 5 years.

If the narrative on China and the company itself improves, then it might trade at 15+ PE. In that case, returns would be 110% total or 16% annual.